The 2026 Crypto Yield Landscape – Why the Rulebook is now Infrastructure

If you are offering, or considering offering, crypto yield in 2026, this is the year the rules stop being theoretical. For years, digital asset regulation has been something to monitor, debate, or anticipate. Now it is operational. MiCA is live. DAC8 reporting has begun. CARF exchanges are scheduled. The U.S. has drawn lines around stablecoin […]

If you are offering, or considering offering, crypto yield in 2026, this is the year the rules stop being theoretical.

For years, digital asset regulation has been something to monitor, debate, or anticipate. Now it is operational. MiCA is live. DAC8 reporting has begun. CARF exchanges are scheduled. The U.S. has drawn lines around stablecoin yield and staking. The rulebook, in other words, is now infrastructure.

The conversation has changed from: “Will regulators allow this?” to “Can your operating model withstand institutional scrutiny?”

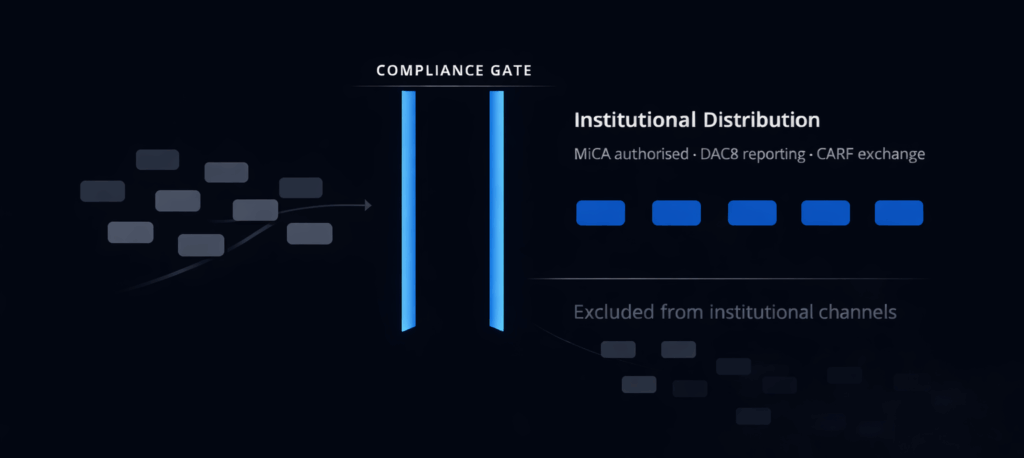

Institutional appetite for crypto yield remains strong, but access is narrowing to regulated players. A Goldman Sachs survey found 35% of institutions cited regulatory uncertainty as the primary barrier. That barrier is being replaced by something more decisive: compliance as a distribution gate. Accordingly, platforms that can evidence segregated custody, position-level reporting, conflict management, and audit-ready infrastructure can compete. Those that cannot will be screened out, competitive yields or not.

At the same time, onchain yield markets have reached real scale. By mid-2025, DeFi lending alone held over $55 billion in TVL, with Aave managing $33 billion and collateralised loans exceeding $26.5 billion. Clearly, the demand and the capital are there. The regulatory clarity is now there.

This article outlines what that means in practice and why the competitive window for MiCA-compliant yield providers is closing fast.

MiCA Imposes Operating Standards Across Europe

MiCA replaces a patchwork of national rules with a single rulebook for crypto asset services. It brings core yield functions, custody, portfolio management, advice, and order execution, into one authorization regime, with supervision anchored in the home state.

For yield businesses, this pushes the market away from black box pooling and toward standards that auditors can test. Articles 66, 70, 72, and 75 raise expectations on conduct, client asset safeguards, conflicts, and position registers, which makes weak attribution harder to defend in regulated distribution.

Practically, this means a platform can no longer simply pool client assets into one large liquidity position. Instead, it needs segregated custody and precise position registers that track each customer’s positions, in a form a compliance team can verify and an auditor can test.

The commercial reward is passporting. Authorization in one member state enables service provision across the EU. When a regulated institution evaluates a yield partnership today, the conversation begins with the custody questionnaire, and without MiCA authorization it ends at the compliance screen.

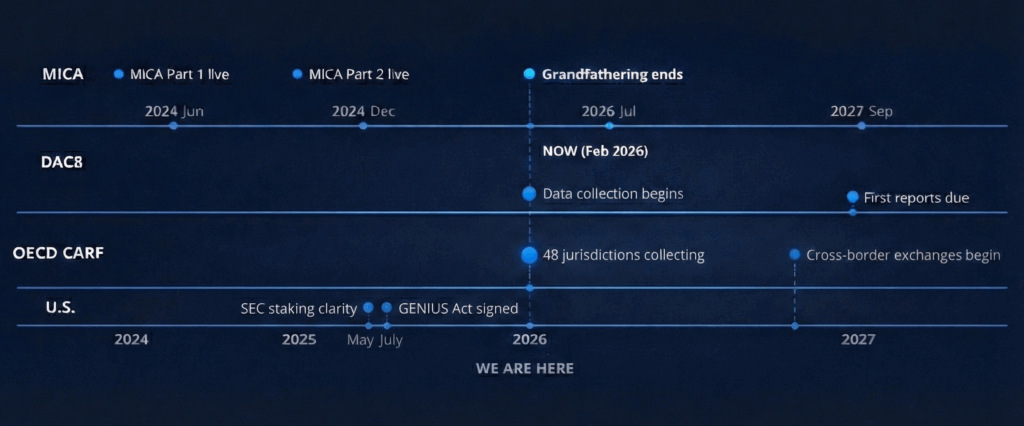

For firms operating under transitional permissions, the grandfathering period varies by member state and can run up to July 1, 2026, with shorter windows in some jurisdictions. As those windows close, compliance becomes a distribution gate, and it narrows the partner field to authorized providers.

Reporting Infrastructure Becomes Mandatory

DAC8 rules took effect on January 1, 2026. First reporting for 2026 activity occurs in 2027, with deadlines set locally. Providers must track transactions, balances, and transfers at the customer level, then exchange that data with tax authorities.

In parallel, the OECD Crypto Asset Reporting Framework has 48 jurisdictions committed, with data collection beginning in 2026 and exchanges from 2027 onward, varying by jurisdiction. For multijurisdiction platforms, this is an operating requirement, not a policy exercise.

Practically, this means yield products need a full transaction ledger that reconciles activity back to individual customer accounts. It also requires collecting and verifying tax identity data, including taxpayer identification numbers and self-certifications, which many legacy onboarding flows never captured. Every deposit, withdrawal, and yield accrual or payment must map cleanly to a customer record that a compliance team can defend and an auditor can test.

The commercial reward is distribution readiness. When a regulated institution asks how yield positions will appear in filings, a provider either has the reporting and reconciliation capability, or it does not.

Stablecoin Yield and Staking Gain Clarity

The GENIUS Act, signed on July 18, 2025, established a federal framework for payment stablecoins in the United States. The legislation prohibits payment stablecoin issuers from paying interest directly to holders, while permitting third party arrangements where platforms deploy assets into lending protocols or treasury instruments, provided custody and reporting standards are maintained.

Structurally, this forces a separation between the asset issuer and the yield provider. Yield can no longer be an opaque feature of the stablecoin itself. Instead, Earn products must be built as distinct, segregated services where the platform deploys stablecoins into protocols while maintaining the custody segregation and reporting transparency that institutional allocators require.

This clarity validates a large addressable market. Stablecoin supply totals over $295 billion as of February 2026, with Tether USDT at $184 billion and Circle USDC at $73 billion. Under the GENIUS Act, issuers cannot pay interest solely for holding a payment stablecoin, while yield can be offered by a service provider through a separate product. In practice, that shifts the opportunity to platforms that can deploy stablecoins into permitted strategies, and keep custody, segregation, and reporting clean enough to pass institutional diligence.

The competitive advantage here is infrastructure maturity. With the U.S. Securities and Exchange Commission staff clarifying the treatment of certain protocol staking activities on May 29, 2025, the gating question shifts from legal classification to operational proof. Providers that can evidence slashing risk controls, uptime performance, and audit ready reporting are better positioned to clear institutional diligence and win mandate.

The Competitive Window Is Closing

MiCA grandfathering ends July 1, 2026. DAC8 data collection became operational January 1, 2026. CARF exchanges begin in 2027 across committed jurisdictions. Authorization processes require months to complete. Providers beginning compliance architecture in mid 2026 will not meet July deadlines.

This creates a window where authorized providers face reduced competition for institutional partnerships. The market is separating into two groups. One group meets MiCA operating standards, handles DAC8 reporting requirements, and operates CARF data exchange systems. These providers can offer regulated DeFi yield services to institutional partners and European Union customers. The other group lacks authorization or reporting capabilities and faces exclusion from institutional distribution channels regardless of underlying protocol quality or rate competitiveness.

These are permanent operating standards for institutionally accessible regulated crypto yield services. When a custody RFP asks for MiCA authorization status, evidence of transaction reporting capabilities, and documentation of conflicts management procedures, only one group can respond affirmatively.

The platforms that operationalize compliance infrastructure now control institutional distribution in this market cycle.